Paid-link disclosure: We may earn a commission from some provider links on this site. Rankings are based on published editorial criteria, not commission rates. This site is educational only and does not provide individualized financial, investment, tax, legal, insurance, Medicare, or Social Security advice. Read our disclosure and editorial standards.

Small Account Guide · $5K–$50K · 2026

Best Gold IRA Companies for Small Accounts

The flat fees that are a rounding error on a $100K rollover become a 2.25% annual drag on a $10K account. This guide is built for you — with the honest ETF math, the fee-drag tables, and the five providers that actually passed our small-account screen.

By The Retirement Index Editorial Team

Published ·Last reviewed ·Fact-checked·Cites IRS, SEC, FINRA, CFPB

Affiliate disclosure: We may earn a commission when you request a free info kit or open an account through links on this page. These commissions support our editorial work but do not influence which companies we recommend. See our full disclosure and editorial standards.

The short answer

For small accounts in 2026, the best Gold IRA companies are Birch Gold Group (publishes a $5,000 minimum and a full $235/year fee schedule on its own site), American Hartford Gold (verified $10,000 minimum; recurring fees must be confirmed in writing), and Lear Capital (verified $10,000 minimum with the full fee schedule online). If your balance is under about $9,000 and you mostly want gold price exposure, a low-cost gold ETF inside your existing IRA is mathematically cheaper than the $225–$275/year flat-fee structures every physical Gold IRA on this page uses — and we’ll show you the math below. At $25,000+, Goldco enters the picture. At $50,000+, Augusta Precious Metals becomes available and you’re not a small account anymore.

Stick with us. Five minutes here will save you from a fee structure you’d regret for ten years.

Verification Log

What we actually verified for this page

✓12 Gold IRA providers screened on published minimum, fee transparency, BBB rating and complaint pattern, custodian and depository disclosures, and a documented regulator-search check across CFTC press releases, SEC litigation releases, state DFPI announcements, and BBB profiles.

✓Provider minimums and fees verified May 2026 from each provider's own published page or fee schedule. Where a provider doesn't publish full recurring fees, we say so plainly and mark it "quote required."

✓2026 IRS rules sourced from IRS Notice 2025-67, IRS Publication 590-A, IRS Publication 17, and IRS guidance on collectibles in qualified plan accounts.

✓ETF expense ratios sourced from the issuer (BlackRock for IAU and GLDM; State Street for GLD).

✓BBB ratings and provider standing verified May 20, 2026. These can change. A BBB A+ does not mean a company is complaint-free.

What you still need in writing before funding any account:

Current promotional waivers, exact coin or bar premium over spot price, segregated vs. commingled storage choice, buyback spread, and any account-closing fees. We’ve built a 15-question script below to make that easy.

Affiliate disclosure: We have affiliate relationships with several of the Gold IRA providers featured on this page. We do not earn anything from the gold ETF route or the bullion marketplace paths (APMEX, JM Bullion) recommended for some readers. Affiliate relationships did not determine ranking — published minimums, fee transparency, and our documented regulator-search screen did.

Quick Verdict

Quick verdict by account size

Find your balance band, get the answer, and the rest of this page is your homework.

Your balance

What we’d do

Why

Under $5,000

Skip the Gold IRA for now. Hold a low-cost gold ETF (IAU or GLDM) inside your existing Roth or Traditional IRA at Vanguard, Fidelity, or Schwab.

Flat Gold IRA fees of ~$225/year eat 4.5%+ of your account every year. The ETF route costs 0.10%–0.25% per year in issuer expense ratio.

$5,000–$9,999

Probably still skip — or use Birch Gold Group if physical metal really matters to you. Run the fee-drag calculator first.

At $7,500, a $235/year fee is 3.1% annually. Defensible only if you have a specific reason to own IRA-held physical metal.

$10,000–$24,999

Compare Birch Gold Group and American Hartford Gold. Both are verified small-account-friendly.

Fee drag drops to 1.0%–2.3% in this range. The structure starts to make sense.

$25,000–$49,999

Add Goldco to the comparison.

Goldco's own materials state that $225/year equals 0.90% at $25,000 — the threshold their fee structure is built around.

Augusta's $50,000 minimum kicks in here and premium service tiers become economically reasonable.

The Honest Part — Read This First

When a Gold IRA isn’t the best move — and what is

We need to get this out of the way up front, because if you’re under about $9,000 and fee-sensitive, you deserve to know it before the rest of the page tries to convert you.

We have affiliate relationships with most of the Gold IRA providers we’re about to compare. We don’thave one with Vanguard, Fidelity, or Schwab. We’re telling you anyway: if your balance is under roughly $9,000 and you mostly just want gold price exposure inside a retirement account, holding a low-cost gold ETF inside your existing Roth or Traditional IRA is mathematically cheaper than any of the $225–$275 per year flat-fee structures on this page.

The math in two lines

ETF option

Annual expense ratio

Crossover vs. $225/yr flat fee

Source

iShares Gold Trust (IAU)

0.25%

$225 ÷ 0.25% = $90,000

BlackRock issuer disclosure

iShares Gold Trust Micro (GLDM)

0.10%

$225 ÷ 0.10% = $225,000

BlackRock issuer disclosure

SPDR Gold Shares (GLD)

0.40%

$225 ÷ 0.40% = $56,250

State Street issuer disclosure

Below the crossover balance, the ETF wins on annual holding-fee math. Above it, the Gold IRA’s flat fee starts pulling ahead as a percentage. These figures cover annual holding costs only — they don’t include product premium, buyback spreads, or brokerage trading costs.

What you give up with the ETF route

You give up direct physical ownership. The ETF holds gold in a vault on behalf of all shareholders; you own a share of the trust, not specific bars set aside for you. If physical IRA-held metal is the whole point for you, the Gold IRA is still legitimate. If you just want gold exposure in retirement, the ETF wins on cost.

One more honest note

Gold IRAs are not the cheapest way to get gold exposure in a retirement account. The reason to use one anyway is the structure — IRS-recognized physical bullion held by a qualified custodian at an approved depository under your IRA. That structure has value to a particular kind of retirement saver. We cover Gold IRAs because that saver exists. We won’t pretend they’re the obvious choice for everyone.

Under $9,000 and fee-sensitive? The iShares IAU fund page and your existing IRA broker are your first stop. We earn nothing from it. It’s still the right answer for a lot of readers.

If you’re still here — meaning you’ve decided physical IRA-held metal is what you want — keep going. The rest of this page is built for you.

5 Providers That Passed Our Screen

Which Gold IRA companies are best for small accounts in 2026?

We screened 12 providers. Five passed our small-account filter: a published or directly-confirmed minimum at or under $25,000, fees we could either find published or get in writing, an A+ BBB rating with a manageable complaint pattern, and no current CFTC, SEC, or FTC enforcement action against them as of our verification date.

Important note: Gold IRA dealers are not automatically fiduciary financial advisors, and most metals sales representatives are not securities-licensed. For personalized allocation advice about whether gold belongs in your retirement plan, use a fiduciary advisor or tax professional.

Provider

Verified minimum

Setup / one-time

Annual recurring fee

Fees published?

BBB

Best for

Birch Gold Group#1

$5,000

$50 setup + $30 wire

$235/yr published ($110 storage + $125 management)

Yes — full schedule

A+

Most $5K–$25K accounts. Best fee transparency.

American Hartford Gold

$10,000

Varies — confirm in writing

Quote required. AHG FAQ states storage varies. Third-party reports ~$225/yr, but not published.

Partial — minimum yes, full fee schedule no

A+

$10K–$25K investors who will confirm fees in writing.

Lear Capital

$10,000

$50 application

$235/yr published (commingled) / $285 segregated

Yes — full schedule

A+

Investors who want platinum or palladium. See regulatory note below.

APMEX (marketplace IRA)

$2,000 IRA purchase minimum

Varies by custodian

Custodian/storage fees separate; confirm with chosen custodian

Partial (varies by custodian)

A+

Lowest verified IRA purchase entry point. Requires separate custodian.

What changes at $25,000: Goldco enters the comparison. Their own materials state that $225/year equals 0.90% at $25,000 — the threshold their fee structure is built around.

What changes at $50,000:Augusta Precious Metals enters. Augusta is excellent for larger accounts, but their $50,000 minimum means they aren’t a small-account option regardless of service quality.

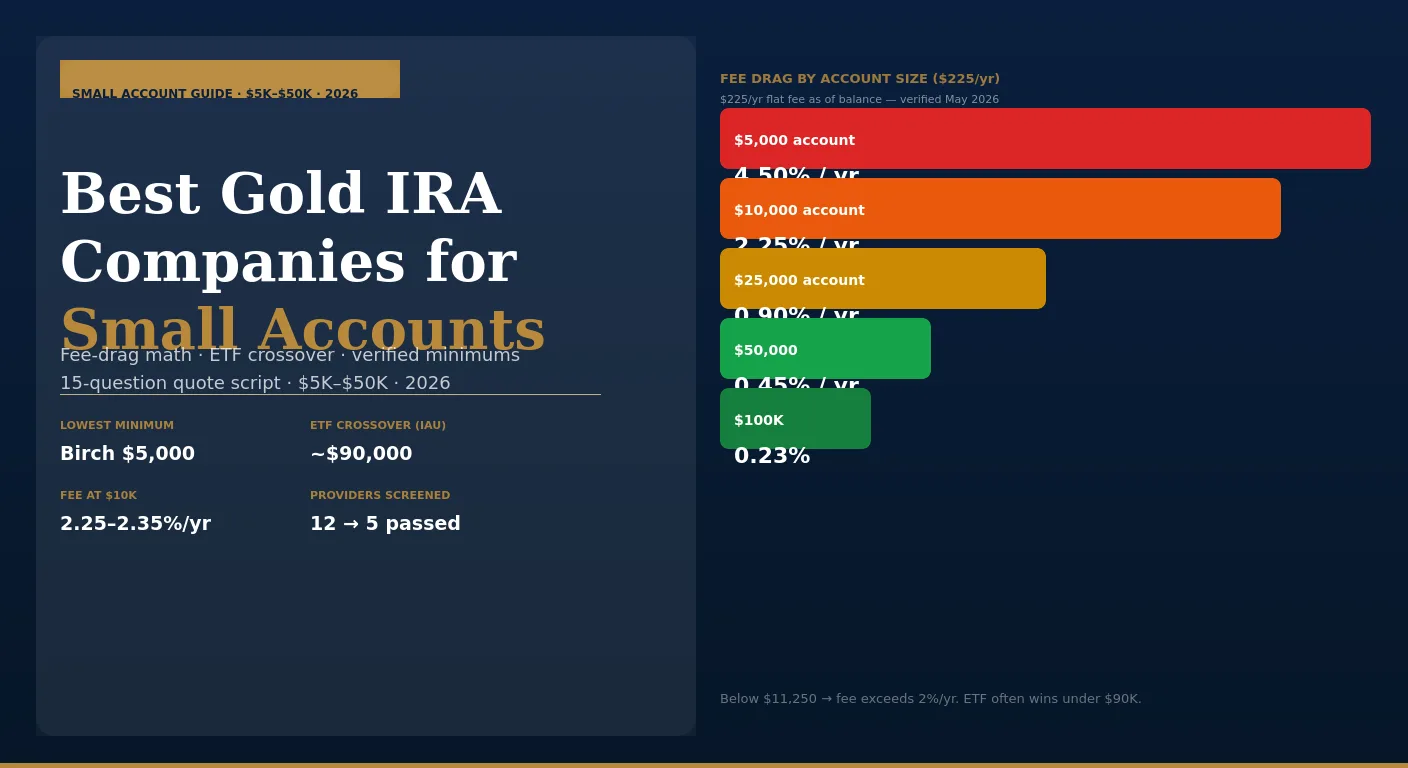

The fee drag table — where small Gold IRAs really hurt

Gold IRAs charge flat dollar fees, not percentage-of-assets fees. That sounds neutral until you do the division.

Table 1: flat fee as a % of account balance

Annual fee

$5,000 acct

$10,000 acct

$25,000 acct

$50,000 acct

$100,000 acct

$180/year

3.60%

1.80%

0.72%

0.36%

0.18%

$225/year

4.50%

2.25%

0.90%

0.45%

0.23%

$235/year (Birch/Lear)

4.70%

2.35%

0.94%

0.47%

0.24%

$275/year

5.50%

2.75%

1.10%

0.55%

0.28%

$300/year

6.00%

3.00%

1.20%

0.60%

0.30%

Red = above 2%/yr. Orange = 1%–2%/yr. Green = under 1%/yr.

Table 2: balance required to keep fee under a threshold

This is the table no other “best gold IRA” page shows you, and it’s the single most useful chart on this page.

Annual flat fee

Balance to keep fee < 2%/yr

Balance to keep fee < 1%/yr

Balance to keep fee < 0.5%/yr

$225/year

$11,250

$22,500

$45,000

$235/year

$11,750

$23,500

$47,000

$275/year

$13,750

$27,500

$55,000

$300/year

$15,000

$30,000

$60,000

Four practical breakpoints from that table

▸Under $11,250: every meaningful Gold IRA's flat fee is costing you more than 2% per year, every year, before you've bought a single coin.

▸$22,500–$23,500: roughly the line where fee drag drops under 1% — the point at which a Gold IRA stops being "expensive" and starts being "reasonable."

▸$45,000–$60,000: the line where flat fees fall under 0.5% of account value.

▸Above $90,000: the IAU crossover. Below this, the ETF is cheaper on annual holding cost. Above $225,000: the GLDM crossover, where even the cheapest gold ETF loses to a flat-fee Gold IRA on holding costs alone.

That’s not opinion. That’s division. And it’s why “best for small accounts” cannot just mirror “best overall.”

Provider Deep Dives

Provider deep dives — ranked for small accounts only

Each profile leads with who it fits, who it doesn’t, and one honest drawback. Every fee number was verified May 2026. Confirm everything in writing before funding — promotions and fee schedules change.

1 — Best Overall for Small Accounts · $5K+

Birch Gold Group — best overall for small accounts

Use Birch if you have $5,000 to $25,000 and you want to see every fee in writing before you talk to a salesperson.

Birch is one of the only major Gold IRA companies that publishes its full fee schedule on its own website. Before you call, you can see that you’ll pay a $50 account setup, a $30 one-time wire fee, $110 in annual storage/insurance, and $125 in annual management — a flat $235 per year going forward. The published $5,000 starting recommendation is the lowest among full-service providers we’d actually trust at this balance level.

Item

Verified detail

Verified minimum

$5,000 recommended starting point (Birch-published)

Metals offered

Gold, silver, platinum, palladium (all four IRS-approved)

One-time costs

$50 setup + $30 wire = $80 total

Annual storage/insurance

$110 (published)

Annual management

$125 (published)

Annual total

$235/year flat (published on birchgold.com)

Fee waiver note

First-year fees paid on transfers of $50,000+ — irrelevant for small accounts, disclosed for completeness

Custodians

Equity Trust Company, STRATA Trust

Depositories

Delaware Depository, Brink's Global Services

BBB (verified May 2026)

A+ rating; accredited since 2013. No federal enforcement actions identified.

Trustpilot (verified May 2026)

4.7/5

Fee drag at $10,000

$235 ÷ $10,000 = 2.35%/yr

Fee drag at $25,000

$235 ÷ $25,000 = 0.94%/yr

The honest drawback

At $5,000 to $8,000, the math still doesn’t strongly favor physical metal over a gold ETF. Birch is the best option if you’ve already decided you want IRA-held physical metal — not the reason to make that decision at a small balance.

Full fee schedule is published online before any phone call. Verify all fees in writing before funding.

2 — Best Full-Service for $10K–$25K

American Hartford Gold — best full-service for $10K–$25K

Use AHG if you have $10,000 to $25,000, want a guided rollover process, and are willing to confirm fees in writing before funding.

American Hartford Gold verifies a $10,000 IRA minimum in its own FAQ. The full fee structure is not published publicly— AHG’s official FAQ states storage fees vary by account size and metal holdings. Third-party sources typically report combined fees around $225/year, but we mark this as “quote required” because we can’t verify the number from AHG’s own public materials.

Item

Verified detail

Verified minimum

$10,000 (AHG FAQ-published)

Metals offered

Gold, silver, platinum, palladium

Setup fee

Varies — confirm in writing

Annual fee

Quote required. Third-party reports ~$225/yr — confirm current terms in writing.

Fees published online?

Partial — minimum yes, full fee schedule no

$50K+ promotion

1 year free storage (advertised) — verify current terms in kit

$100K+ promotion

Multi-year storage waiver (advertised) — verify current terms in kit

Metals variety

All four IRS-approved metals (gold, silver, platinum, palladium)

BBB (verified May 2026)

A+ rating; accredited since June 2016.

The honest drawback

AHG doesn’t publish its full recurring fee schedule. That’s a meaningful transparency gap compared to Birch. Before calling AHG, use the 15-question script below and get all fees confirmed in an email before any paperwork.

Best for:$10K–$25K investors who want a full-service guided rollover and are willing to do the written-quote homework. If you won’t push for written fees, use Birch instead — the fee schedule is already in front of you.

3 — Published Fees · Platinum & Palladium · $10K+

Lear Capital — published fees and all four metals at $10K

⚠ Read the regulatory history before deciding

Lear Capital has a settled regulatory history that is material disclosure for any buyer. In 2022, Lear settled $6 million with the New York Attorney General over alleged failure to disclose that approximately one-third of investor funds would go to commissions. In 2022, Lear filed for bankruptcy protection. In 2023, Lear reached a $5.5 million multi-state bankruptcy settlement covering investors from 2016–2022; at least 42 state and territory securities regulators had been investigating Lear. We include Lear here because the MD that governs this page includes them on the basis of fee transparency and published schedule — and because the regulatory history, including a post-settlement pledge not to misrepresent fees, is the reason the full fee schedule is published today. Make your own judgment about whether that history is disqualifying for your situation.

Item

Verified detail

Verified minimum

$10,000 (Lear-published)

Metals offered

Gold, silver, platinum, palladium

Application fee

$50 (published)

Annual fee (commingled)

$235/year (published)

Annual fee (segregated)

$285/year (published)

Fees published online?

Yes — full schedule on learcapital.com/knowledgebase/fee-and-transparency/

BBB (verified May 2026)

A+ rating (current rating as of verification date)

Regulatory history

2022 NY AG $6M settlement; 2022 bankruptcy; 2023 $5.5M multi-state settlement. See disclosure above.

Best for: Small-account investors who specifically want platinum or palladium options and want a published fee schedule — and who have read the regulatory history and made their own judgment about it.

Not for:Investors who aren’t comfortable with the settled regulatory record. Birch Gold Group has a comparable published fee schedule, comparable annual cost, and a cleaner regulatory record.

4 — Enters at $25K · Bonus Metals Tier

Goldco — enters the comparison at $25,000

Goldco’s own materials explicitly state that $225/year equals 0.90% at $25,000 — which is exactly why that’s their general floor. If you’re below $25,000, Goldco isn’t the right call. At $25,000 to $49,999, Goldco belongs in your shortlist alongside Birch because they’ve built their economics around exactly this balance band.

Item

Verified detail

General minimum

$25,000

Metals offered

Gold and silver only

Annual fee

~$225/yr; Goldco publishes a cost example on goldco.com/how-much-does-a-gold-ira-cost/

Fee at $25K

$225 ÷ $25,000 = 0.90%/yr (Goldco's own stated threshold)

Bonus metals tier

Up to 5% in free metals on qualifying $50K+ premium-coin purchases; up to 10% at $100K+ (terms apply — read before assuming net value)

BBB (verified May 2026)

A+ rating; accredited since 2011.

Best for: $25,000–$49,999 investors who want a guided rollover experience and are interested in comparing bonus-metals economics. Below $25,000, start with Birch.

5 — Marketplace Paths · Lowest Entry Points

APMEX and JM Bullion — marketplace IRA paths for lowest minimums

These are bullion marketplaces, not full-service Gold IRA companies. You choose your own custodian and depository separately.

Provider

IRA minimum

What you get

What you arrange separately

APMEX

$2,000 IRA purchase minimum

Wide selection of IRA-eligible bullion; competitive premiums over spot; A+ BBB

Custodian (e.g., Equity Trust), depository, IRA setup — APMEX is the dealer only

JM Bullion

No IRA-specific minimum beyond $100 general order minimum

Competitive premiums; wide bullion selection; IRA FAQ on site; A+ BBB

Custodian, depository, IRA structure — JM Bullion is the dealer only

The honest tradeoff

Marketplace paths offer the lowest entry points and often competitive product premiums, but they require you to separately choose and contract with a custodian and depository. For a first-time Gold IRA buyer without prior SDIRA experience, the coordination burden is a real cost — and the one-stop-shop experience of Birch or AHG has genuine value. If you’re comfortable managing three vendors, the marketplace path can save money on product costs. If not, start with a full-service provider.

Know your number — request written quotes

Request written quotes from two providers on the same day using the same product specs. Compare premium percentages and all-in cost using the 15-question script below.

Sell via dealer; usually 1–5 business days at buyback spread

Sell on exchange instantly during market hours

Tax treatment in IRA

Same as regular IRA

Same as regular IRA

Tax treatment outside IRA

Collectibles gain rules (max 28%) for long-term; short-term is ordinary income — confirm with CPA

Many physically backed trusts treated similarly — confirm with fund prospectus and CPA

When the ETF wins on cost

✓Balance under $25,000–$30,000 (percentage drag of flat fees still meaningful)

✓No specific reason you need physical IRA-held metal vs. trust-held

✓You value setup speed and liquidity

✓You don't want to manage three vendors (dealer + custodian + depository)

When physical Gold IRA may fit better

✓Balance high enough that flat fees become a small % (~$25K minimum, ideally $50K+)

✓You specifically want IRA-held bullion at a depository, not a share in a trust

✓You want the option to take physical metal as in-kind distribution after age 59½

✓You're comfortable with additional fees in exchange for the structure

The hybrid route many small-account investors consider: Hold IAU or GLDM inside an existing IRA now, then evaluate a physical Gold IRA once the balance grows past about $25,000. For many readers, this is the most defensible path.

IRS Rules — Non-Negotiable

2026 IRS rules every Gold IRA holder needs to know

Three rules govern every Gold IRA, regardless of provider, balance, or how aggressive the salesperson is.

Rule 1 — 2026 contribution limits

For 2026, the IRS allows total IRA contributions of $7,500 per year, or $8,600 if you’re age 50 or older (a $7,500 base plus a $1,100 catch-up). These limits apply across all your IRAs combined — Traditional, Roth, and Gold IRAs share the same annual cap. For small accounts, building a Gold IRA from annual contributions alone is slow. A $7,500 contribution against $225 in annual fees burns 3% of your contribution to fees in year one. Most small Gold IRAs are funded by rollovers from old 401(k)s or existing IRAs.

Source: IRS Notice 2025-67; IRS Pub 590-A

Rule 2 — Eligible metals (purity standards)

The IRS requires metals held in an IRA to meet specific purity standards: Gold must be at least 99.5% pure (American Gold Eagles are an explicit statutory exception at 91.67%); Silver at least 99.9%; Platinum and palladiumat least 99.95%. Common IRS-approved options include American Gold Eagle, Canadian Maple Leaf, Australian Kangaroo, and IRS-eligible bars from approved refiners. Collector coins, jewelry, and “rare” numismatic coins generally do not qualify — they’re also one of the most common scam vectors in the industry.

Source: IRS guidance on collectibles in qualified plan accounts; IRC §408(m)(3)

Rule 3 — Storage (no home storage, ever)

IRS rules require IRA-eligible bullion to be in the physical possession of a bank or approved nonbank trustee. You cannot legally store IRA gold at home— not in a safe, not in a bank safe deposit box held personally, not through an LLC marketed as a “Home Storage Gold IRA.” The leading case is McNulty v. Commissioner, 157 T.C. No. 10 (2021), where the IRS assessed income tax deficiencies of $250,558 and $18,094 for 2015 and 2016, plus accuracy-related penalties, after the taxpayers personally possessed IRA-owned American Eagle coins through an LLC structure. Any company pitching “Home Storage Gold IRA” or “Self-Held IRA” — walk away immediately.

Source: IRS.gov on collectibles in IRAs; McNulty v. Commissioner, 157 T.C. No. 10 (2021)

Step-by-Step

How to open a small Gold IRA without overpaying — 5 steps

Don’t skip any. Do them in this order.

1

Decide if you actually want physical IRA metals

If your honest answer is "I just want gold exposure in my retirement account," stop here and use IAU or GLDM in your existing IRA. The Gold IRA path is for people who specifically want IRS-recognized physical bullion held in custody at an approved depository.

2

Run the fee-drag math at your balance

Enter your starting balance and a $225 default fee into the fee-drag table above. If the year-1 drag is over 2.5%, the math is telling you to wait or use an ETF. If you're committed anyway, proceed.

3

Shortlist by balance band

Use the quick-verdict table at the top of this page. Don't waste a call on Augusta if you have $12,000. Don't call Goldco if you have $8,000. Match provider to balance band.

4

Request written quotes from at least two providers

Use the 15-question script below. Compare in writing. The cheapest minimum sometimes hides the most expensive markup — specifically the premium over spot on the metals you'll buy on day one.

5

Fund only after you have everything in writing

Use a direct rollover or trustee-to-trustee transfer wherever eligible — it avoids the 60-day rollover deadline and the 20% federal withholding on employer-plan distributions paid to you. Confirm the metals were received at the depository. Get the account statement and the depository inventory confirmation before you consider the transaction complete.

What Real Small-Account Investors Worry About

The real questions behind the Google searches

The most common questions we see across retirement forums (Bogleheads, Reddit personal-finance, AARP community threads, BBB review notes) aren’t about which company has the shiniest brochure. They’re about whether the math works at all:

▸Whether a small balance — sometimes as low as $1,000 — is even worth a Gold IRA

▸Whether smaller investors get taken seriously by Gold IRA companies built for six-figure rollovers

▸Worry about fees, storage, and rollover mechanics specifically

▸Hedging inflation without giving up too much of the account to flat annual costs

The honest read: small-account Gold IRA investors are fee-aware, slightly distrustful of the industry’s marketing, and tired of feeling like the financial industry only takes them seriously above $100,000. You’re not “small money” to us — you’re someone making a structural retirement decision under different math than the six-figure crowd, and you deserve a real answer. This page is that answer.

Before You Fund Anything

The 15-question written quote script

Every answer on this list should be provided in writing — in an email or document — before you authorize any funds transfer. On a five-figure account, verbal promises aren’t enforceable. If a dealer refuses to answer any of these in writing, walk away. Compare responses from at least two providers on the same day, using the same product specifications.

1What is the exact product you're selling me? (Coin name, weight, purity, mint — not just "gold coin")

2What is today's spot price you're using as your reference? (Dollar and date/time)

3What is the price per coin or per bar you're charging me?

4What is the percentage premium (markup) over spot — expressed as a percentage?

5What is the total purchase cost in dollars for my entire order?

6Is this standard bullion, a premium coin, or a numismatic product? If premium — what is the standard bullion premium-over-spot for comparison?

7What are all one-time setup costs — account setup, wire fees, application fees — itemized separately?

8What are all annual recurring fees — custodian and storage — itemized separately? Is storage commingled or segregated, and what is the price difference?

9Who is the IRA custodian? What is their legal entity name, and what is their annual fee in writing?

10Who is the depository? What is the legal name, physical location, insurance carrier, and coverage amount?

11Does any current promotion or fee waiver apply to my account? What are the exact terms and qualification requirements in writing?

12What is the buyback process? What is the current bid price for this specific product today? Is buyback guaranteed or at your discretion?

13Are there any liquidation fees, account-close fees, or in-kind RMD distribution fees?

14What is the estimated time from paperwork submission to metals held at the depository?

15Can you confirm all of the above in writing via email before I authorize any wire transfer or rollover paperwork?

The rule: if it’s not in writing, it didn’t happen

“Free silver” verbal offers, verbal fee waivers, verbal buyback guarantees — none of these are enforceable. On a $10,000–$25,000 account, a 4% markup difference is $400–$1,000. That’s more than a full year of fees. Get every commitment in email before any money moves. The five minutes that takes is the single best protection against the patterns the CFTC has been prosecuting for a decade.

FAQ

Frequently asked questions — small Gold IRA accounts

What is the minimum investment for a gold IRA in 2026?

▼

There is no single industry minimum — each provider sets its own. The lowest verified entry points in 2026 are APMEX at $2,000 (IRA purchase minimum at a bullion marketplace), Birch Gold Group at $5,000 (recommended starting point, Birch-published), American Hartford Gold and Lear Capital at $10,000, Goldco at $25,000, and Augusta Precious Metals at $50,000. At balances under $10,000, the fee drag often makes a gold ETF in an existing IRA the more economical structure.

Can I open a gold IRA with $5,000?

▼

Yes — Birch Gold Group publishes a $5,000 recommended starting point on its own site, and bullion marketplace paths like APMEX accept IRA purchases starting at $2,000. However, at $5,000, a typical $225/year Gold IRA fee equals 4.5% annual drag before any metal markup. For most $5,000 investors, a gold ETF inside an existing IRA is the better starting structure — unless you have a specific reason to need IRA-held physical metal.

Can I open a gold IRA with $10,000?

▼

Yes, and $10,000 is where the structure starts to make practical sense. American Hartford Gold, Birch Gold Group, and Lear Capital all accept $10,000 accounts with verified published or quote-confirmed fees. Annual fee drag at $10,000 is typically 2.25%–2.35% — high relative to a regular IRA, but defensible if physical metal in an IRA structure matters to you specifically.

Is a gold IRA worth it under $25,000?

▼

Sometimes. Below about $9,000, the math almost always favors a gold ETF in your existing IRA. Between $10,000 and $25,000, a Gold IRA is defensible if direct physical ownership matters and you're using a low-minimum provider with published fees. Above $25,000, more providers become available and the percentage drag of flat fees becomes more manageable. At $25,000 specifically, $225/year equals 0.90% — Goldco's own stated threshold for that reason.

Which gold IRA company has the lowest minimum?

▼

Among major full-service providers, Birch Gold Group publishes the lowest minimum at $5,000. APMEX has the lowest verified IRA purchase minimum at $2,000, but APMEX is a bullion marketplace — you'd need to arrange the custodian and depository separately.

Are gold IRA fees tax-deductible?

▼

No. IRS Publication 17 states that trustees' administrative fees billed separately and paid in connection with a traditional IRA are not deductible as IRA contributions and are not deductible as itemized deductions. Confirm treatment with a CPA for your specific situation.

Can I store gold from a gold IRA at home?

▼

No. The IRS requires IRA-eligible bullion to be in the physical possession of a bank or approved nonbank trustee. The McNulty v. Commissioner, 157 T.C. No. 10 (2021) case demonstrated the cost of getting this wrong — income tax deficiencies of $250,558 and $18,094 for 2015 and 2016, plus accuracy-related penalties, for one Rhode Island couple who stored IRA gold at home through an LLC structure. Any company marketing a "Home Storage Gold IRA" or "Self-Held IRA" is advertising something that exposes your account to IRS reclassification as a taxable distribution.

Gold IRA vs. gold ETF: which is better for a small investor?

▼

For balances under roughly $9,000, a gold ETF (IAU at 0.25% or GLDM at 0.10%) held inside an existing Roth or Traditional IRA is mathematically cheaper on annual holding cost. The crossover where the Gold IRA's flat fee wins is approximately $90,000 vs. IAU and $225,000 vs. GLDM. Between those points, the ETF is cheaper on percentage, but a physical IRA structure gives you titled physical metal and an in-kind distribution option at retirement. For small accounts, the ETF is the cost winner — the Gold IRA is the structure winner for buyers who specifically need that structure.

What's the difference between a Roth Gold IRA and Traditional Gold IRA?

▼

The metals and fees are identical — the tax treatment differs. Traditional Gold IRA contributions may be deductible if income and workplace-plan rules allow (rollovers are not new deductible contributions). A Roth Gold IRA is funded with after-tax dollars; qualified withdrawals including gains are tax-free after age 59½ and a five-year holding period, with no required minimum distributions during the original owner's lifetime. Source: IRS RMD FAQs. Tax law changes — verify current rules with a CPA.

Which gold coins qualify for a gold IRA?

▼

Gold must be at least 99.5% pure to qualify, with American Gold Eagles a statutory exception at 91.67%. Common IRS-approved options: American Gold Eagle, Canadian Maple Leaf, Australian Kangaroo, and IRS-eligible bars from approved refiners. Numismatic, "rare," and most collectible coins are not IRA-eligible — they're also one of the most common upsell vectors in the industry.

Can I move my 401(k) into a small gold IRA?

▼

Yes, via a direct rollover or trustee-to-trustee transfer, which avoids the 60-day deadline and, for employer-plan distributions paid to you, the 20% federal withholding problem. Most full-service providers on this page will coordinate the rollover with your existing plan administrator. Rollovers don't count against the annual $7,500 / $8,600 IRA contribution limit — so a rollover is typically how small-balance investors reach a meaningful Gold IRA starting amount.

Are "free metals" or "first-year fees waived" offers real?

▼

Sometimes, but always tied to conditions. "First year fees waived" typically requires a minimum transfer amount — often $50,000 or more, which is above the small-account range. "Free silver" promotions are typically funded through the markup on metals you do purchase. The only way to know whether a promotion is genuinely valuable is to compare the all-in cost — including premium over spot — against a competitor without the promotion, using the 15-question script above.

Final Word

The decision tree

If you came to this page hoping for a single “here’s the best one, click here” answer, here it is:

Under $5,000

Hold IAU or GLDM inside your existing IRA. Come back when your balance is bigger.

$5,000–$9,999

Run the fee-drag table above. If year-1 drag is over 3%, use the ETF route. If physical IRA-held metal is non-negotiable for you, Birch Gold Group is your starting point.

$10,000–$24,999

Compare Birch Gold Group and American Hartford Gold with written quotes. Add Lear Capital if you want platinum or palladium (after reading the regulatory history).

$25,000–$49,999

Add Goldco. Compare three quotes side-by-side using the 15-question script above.

Get every fee in writing before you fund. Use the 15-question script. Don’t take a verbal “we’ll waive that” — make them email it. The five minutes that takes is the single best protection you have against the patterns the CFTC has been prosecuting for a decade.

Still Not Sure?

Get a personalized retirement action plan

Whether the right move is a Gold IRA, a gold ETF, a Roth conversion, or speaking with a fiduciary advisor about whether gold belongs in your retirement strategy at all — take our free 60-second matching tool to get a personalized retirement action plan. No phone calls. No obligations.

And if a gold IRA isn’t the right answer for your situation, you’ll know that before you’ve written a check.