What is the best Gold IRA company in 2026?

+

For rollovers of $50,000 or more, Augusta Precious Metals is our top pick — A+ BBB, $50,000 published minimum, no management fees, and an education-first sales process. For $10,000–$50,000 rollovers, American Hartford Gold is our top comparison candidate based on its $10,000 minimum and competitive fee structure. For all four metals at a lower minimum, Birch Gold Group publishes a verified $5,000 minimum with an itemized fee schedule. See the full comparison table above for a side-by-side view.

What is a Gold IRA?

+

A Gold IRA is a self-directed Individual Retirement Account that holds IRS-approved physical precious metals — gold, silver, platinum, and palladium — instead of stocks, bonds, or mutual funds. It follows the same tax rules as any IRA (Traditional or Roth) but requires three separate companies to operate: a dealer (who sells you the metals), an IRS-approved custodian (who administers the IRA per IRC §408 rules), and an IRS-approved depository (which stores the physical metals). The metals are held in the depository's name for the benefit of the IRA — you do not take personal possession.

How much does it cost to start a Gold IRA?

+

A typical Gold IRA costs $25–$80 to open (setup fee) plus $180–$300 in annual custodian and storage fees combined. But the largest cost in your first year is almost always the premium over spot on the metals themselves — typically 5%–10% for standard bullion and, per the CFTC, 40%–200% on numismatic or collectible coins. On a $50,000 rollover, that premium can range from $2,500 to $25,000+ depending on what product you buy. The quote worksheet above breaks down all five cost components.

What is the minimum to open a Gold IRA?

+

Published minimums in 2026 range from $5,000 (Birch Gold Group) to $50,000 (Augusta Precious Metals and U.S. Gold Bureau). American Hartford Gold and American Bullion each publish a $10,000 minimum. Goldco's published general minimum is $25,000. Noble Gold and Preserve Gold require a call for their current IRA minimum. Confirm directly with any provider before assuming.

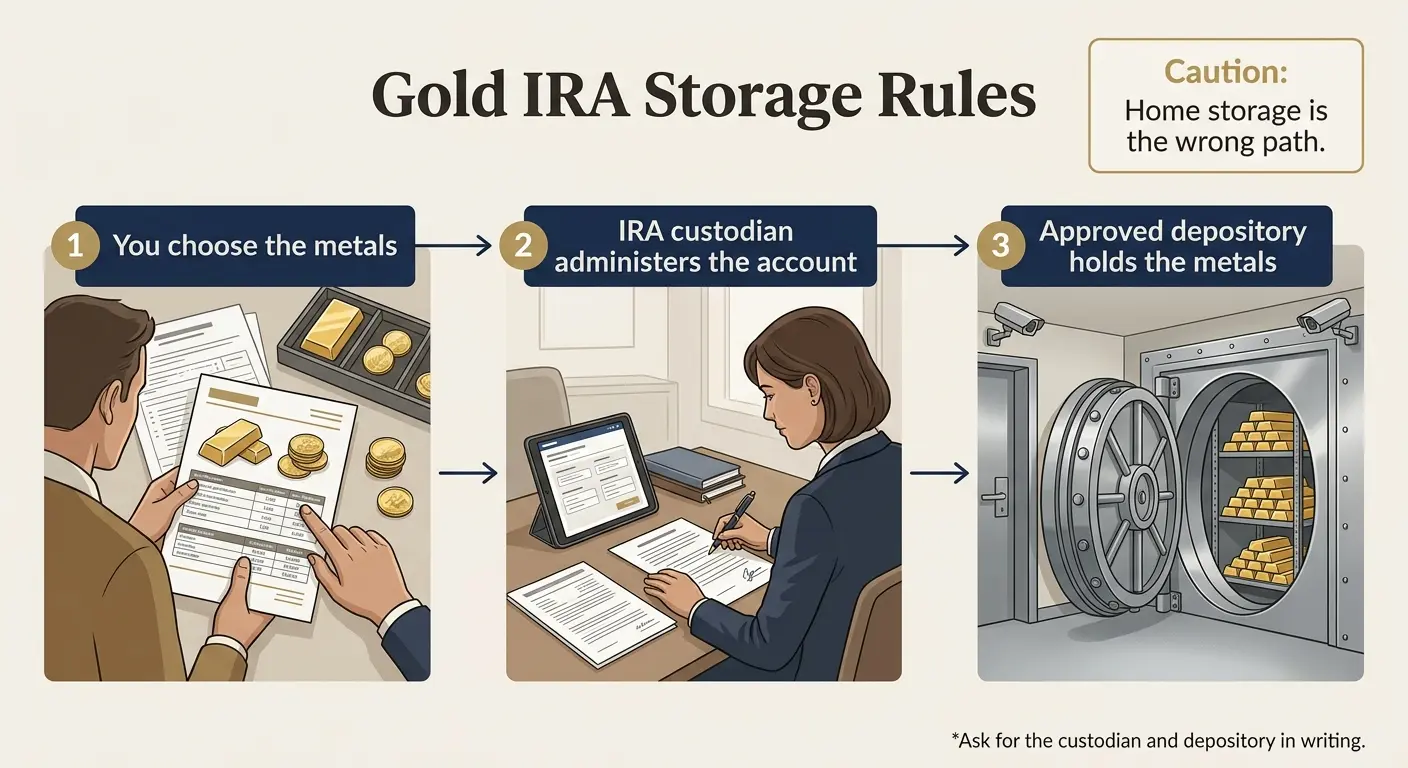

Can I store my Gold IRA metals at home?

+

No. IRS guidance under IRC §408(m) requires that IRA-owned precious metals meeting the bullion exception be held in the physical possession of a bank or IRS-approved nonbank trustee — the depository. Taking personal possession triggers a deemed distribution: full income tax on the value plus a 10% penalty if you are under age 59½. The 2021 Tax Court case McNulty v. Commissioner, 157 T.C. No. 10, confirmed this applies to IRA-owned LLC structures as well. Any company telling you home storage is a simple workaround is misrepresenting IRS rules.

Can I roll over a 401(k) into a Gold IRA?

+

Yes. A 401(k), 403(b), 457, TSP, or existing Traditional or Roth IRA can be rolled over into a self-directed Gold IRA. The cleanest method is a direct trustee-to-trustee transfer — the funds go directly from your current custodian or plan administrator to the new Gold IRA custodian, with no tax event, no mandatory withholding, and no 60-day window to manage. Most Gold IRA providers will coordinate the rollover paperwork. The typical timeline from kit request to funded account is 2–4 weeks.

What is the downside of a Gold IRA?

+

Gold IRAs have higher annual fees than standard stock and bond IRAs ($200–$400/year vs. near-zero at major brokerages), higher transaction costs (5%–30%+ premium over spot on metals vs. fractional pennies for stocks), no income generation (no dividends or interest), and required minimum distributions on Traditional Gold IRAs starting at age 73 (or 75 for later birth cohorts under SECURE 2.0) which can force partial sales or in-kind distributions of metals. They cannot be stored at home. For pure low-cost gold exposure, a gold ETF in a regular IRA is significantly more efficient.

Are Gold IRAs a good investment?

+

There is no universal answer. The SEC, FINRA, and CFTC don't endorse or condemn Gold IRAs as a category — they note that precious metals are often marketed as safe-haven investments but are not immune from price declines and can carry high fees relative to other retirement assets. A Gold IRA may fit an investor who specifically wants physical metals inside a tax-advantaged account and understands the fee structure going in. It is generally a poor fit for small balances (under $10,000) or investors who need easy liquidity. This is not personalized investment advice; consult a fiduciary financial advisor.

What metals are allowed in a Gold IRA?

+

Per IRC §408(m), the IRS treats metals as collectibles with specific statutory exceptions for certain coins and bullion that meet fineness requirements and are held by an IRS-approved trustee. Allowed fineness: gold 99.5%+ (the American Gold Eagle is a separate statutory exception at 91.67% purity), silver 99.9%+, platinum 99.95%+, palladium 99.95%+. Common qualifying products include American Gold Eagle, Silver Eagle, Platinum Eagle, Palladium Eagle coins; Canadian Maple Leafs; and approved bullion bars from COMEX- or LBMA-accredited refiners. Numismatic and collectible coins generally do not qualify.

Who is the best Gold IRA custodian?

+

The custodian is usually assigned by your Gold IRA dealer. The major custodians in this space are Equity Trust Company, STRATA Trust Company, GoldStar Trust, and Horizon Trust. Augusta and Birch Gold most commonly use Equity Trust; Goldco uses STRATA Trust or Equity Trust; American Bullion and Noble Gold use STRATA Trust. Annual custodian fees vary modestly ($80–$160/year across the major custodians). Verify the custodian relationship by contacting the custodian directly — they are regulated entities with public-facing customer service.

Is Augusta Precious Metals better than Goldco?

+

For rollovers of $50,000 or more, Augusta Precious Metals is generally the stronger choice — slower, more education-focused, and the only major provider whose own FAQ states 'no management fees.' For first-time rollovers in the $25,000–$50,000 range, Goldco's $25,000 minimum and recognized brand make it the more accessible fit. Both have clean regulatory records and A+ BBB ratings. The biggest verification ask before funding either: the premium over spot on the specific products being recommended to you, in writing.

Is Birch Gold Group better than Goldco?

+

Birch Gold Group is the better choice if you specifically want platinum or palladium (Goldco is gold and silver only) or if you want a lower published minimum ($5,000 vs. Goldco's $25,000). Goldco is the better choice if you want a guided first-rollover experience at $25,000+ with a more recognized national brand. Both have A+ BBB ratings and clean regulatory records as of May 19, 2026. Birch publishes a more detailed fee breakdown; Goldco's buyback guarantee language is more explicit.

Is Lear Capital safe to use?

+

Lear Capital is currently operating under binding commitments from its 2023 bankruptcy plan, including not to misrepresent fees and not to provide investment advice. It settled with state and territory regulators for $5.5 million as part of the bankruptcy plan and separately with the New York Attorney General for $6 million in 2022 over allegations of undisclosed commissions of up to 33%. Whether the company has fully reformed is a judgment call. We did not rank Lear as a primary recommendation but included it for transparency. If you're considering Lear, compare against Birch Gold's $5,000 minimum with no comparable enforcement history.

Are Gold IRA contributions tax deductible?

+

Traditional Gold IRA contributions may be deductible up to the 2026 annual limit ($7,500, or $8,600 if you are age 50 or older), subject to income phase-out rules if you or your spouse is covered by a workplace retirement plan. Roth Gold IRA contributions are made with after-tax dollars and grow tax-free if qualified distributions. Rollover contributions from a 401(k) or another IRA are not subject to the annual contribution limit. Per IRS IR-2025-111 (November 13, 2025). Tax laws change — verify current rules with a CPA before assuming a specific outcome for your situation.

Is a Gold IRA better than a gold ETF?

+

A gold ETF inside a regular IRA is significantly cheaper than a Gold IRA for pure gold exposure — iShares Gold Trust (IAU) lists a 0.25% annual sponsor fee and SPDR Gold Shares (GLD) lists 0.40%, versus $200–$400 per year in flat Gold IRA fees plus a premium-over-spot at purchase. A Gold IRA is the better choice only if you specifically want physical metals you own outright, held at a named depository in your name, that you could in theory take home at retirement as an in-kind distribution. For cost-efficient gold exposure inside a retirement account, the ETF wins.